Click here to download the financial newsletter in PDF format.

Introduction

Hello everyone,

The second quarter ended on a high note with North American indices setting new record highs. As has been the case from the firm’s beginnings, our clients’ savings are growing at a rapid pace and continue to outperform benchmark indices by several percentage points. However, since the beginning of 2014, a 5% increase of the Canadian dollar against the U.S. dollar resulted in a slight decline in our “outperformance” by the same number of percentage points. In our opinion, these fluctuations will adjust themselves automatically over the long-term, so we expect this to be temporary.

Where the company is concerned, the second quarter was much busier. Firstly, the conversion of our clients’ assets to the National Bank following the acquisition of TD Waterhouse Institutional Services on June 13 was quite a feat. The process went smoothly and the only thing left to do is to accurately track the history of each of the accounts in our portfolio management system. Because of this, the newsletter won’t outline the details of our performance in the most recent quarter. The data needed to calculate the indices has not yet been verified against-NDEX Systems, our independent external platform. We will post the returns as soon as possible in a specific tab on our website. However, our customers can rest assured that the last three months have again been quite successful.

Recent weeks have also been very exciting as it relates to the design of new products to meet the growing needs of our expanding clientele. As many already know, our best-performing strategy in recent years is the Absolute Return Strategy, with a yield of nearly 20% annualized. I am extremely proud to announce the creation of the first ever investment fund to be managed in the Outaouais region, the Rivemont Absolute Return Fund, which will be active as of January 1, 2015. The fund will be based on the above-mentioned strategy and will be available to all of our clients as well as to institutions such as pension funds and private foundations.

The first part of this letter will address in more detail the reasons behind the creation of this fund and the benefits of holding such assets in a diversified portfolio. In the second part, I will discuss some of the basic theoretical notions we used, referring in particular to the work of James Tobin, Nobel Laureate in Economics, to build a high performing portfolio that respects the individual risk profiles of our clients. The latter section of the newsletter was co-authored by Marie-Ève Drolet-Mailhot who worked with us this summer as a junior investment analyst. As usual, I will conclude with our outlook on markets and the composition of our current portfolio. .

Happy reading!

Rivemont Absolute Return Fund

After a rise like the one we witnessed in the markets over the past five years, it is normal to have to discuss with our customers how we will react to the eventual decline in North American markets. Fortunately, private management allows us to underweight assets that we believe are most at risk, avoid certain areas with less potential and even transfer a portion of a portfolio abroad. However, being underweight in certain assets does not allow us to profit from the downward movement of the markets. An absolute return strategy includes so-called “short selling”, a technique to take advantage of the declining price of an asset. With this approach, performance is no longer directly correlated to the market, but more related to the manager’s ability to seize opportunities that arise and capitalize on industry trends as they extend upward or downward.

Potentially avoiding losses in more difficult years, the portfolio is more stable, less volatile and therefore much more advantageous to the investor. Unfortunately, this type of strategy has not typically been accessible to “ordinary” customers; i.e. those who do not have access to the so-called alternative strategies valued by institutions and the very wealthy. This month, Forbes magazine published details of the investments of American billionaires, courtesy of the Swiss bank UBS, which has relationships with over half of the world’s billionaires.

At the outset, it appears that the most affluent American investors use alternative approaches to place nearly a quarter of their assets in hedge funds and private equity. The reason is simple: although these investors hope to continue to enrich themselves, the emphasis is on preserving capital and reducing volatility. These alternative strategies therefore provide effective support when other portfolio assets, such as stocks and bonds have a lower yield.

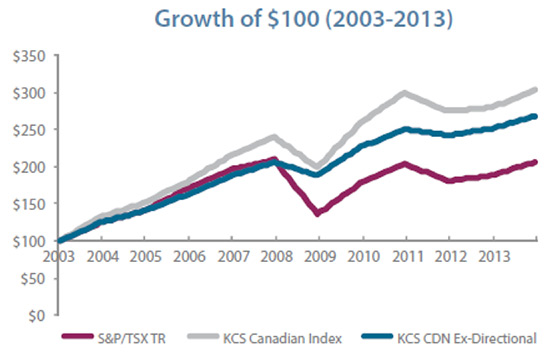

The most recent newsletter of the Alternative Investment Management Association includes an interesting analysis by KCS Fund Strategies. The firm has created a benchmark comprising about 200 Canadian hedge funds. From the outset, this study comes to the conclusion that it is much less risky to invest in these funds than in the index.

We see that in 2008, the worst year in the past decade for stocks on the Toronto Stock Exchange, hedge fund index investors’ losses were only half those of the S&P/TSX, while gains were similar for the best year, 2009. Moreover, investors in hedge funds recovered their capital twice as fast after the crisis, indicating that this strategy yielded the expected results.

Rivemont Investments decided to offer its customers, and certain accredited investors, the Rivemont Absolute Return Fund, the only investment fund managed in the Outaouais region and one of the few funds managed in Quebec. We will be able to offer our customers innovative, exclusive and profitable strategies that cannot be found anywhere else.

The previous section on the Rivemont Absolute Return Fund was purely informative and should not be regarded as financial advice or solicitation.

A Customized Portfolio

The second issue that I will address came to mind after the first meeting with a potential client a few months ago. The latter, a prosperous professional, also deals with the assets of his parents, who are obviously much older than him. When collecting personal information, he clearly suggested to me that he did not want his stocks to be identical to those of his parents. In fact, he wanted his portfolio to consist of more aggressive stocks, while his parents’ portfolio would have more defensive stocks. Although this approach to portfolio management is common, it is highly damaging to both aggressive and conservative investors.

It should be understood that a large portion (90%) of portfolio risk and return potential is related to the weighting of asset classes in the portfolio, not individual positions within each of these categories. Thus, a well-diversified portfolio with equal shares of stocks and bonds, will always be less volatile in the medium term than a portfolio containing only stocks. And if we take into account the tax aspect (capital gains are taxed less than dividends), then it is clear that we must choose stocks according to their potential for possible gain and not according to their historical volatility or their dividends, particularly since modern businesses often favor stock buyback.

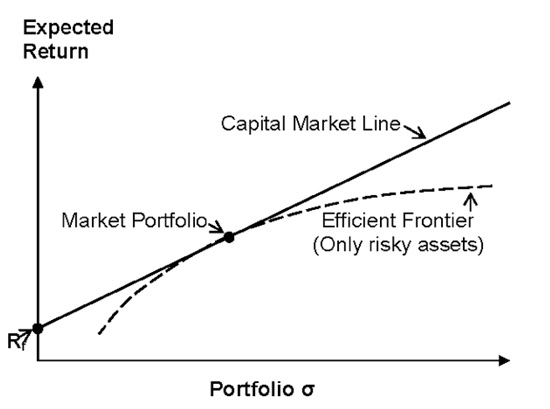

James Tobin, an American economist who received the Nobel Prize in Economic Sciences in 1981 for his article entitled “Liquidity Preference as Behavior Towards Risk,” demonstrates in theoretical terms the approach that we advocate. The author is known for the Separation Theorem, published in 1958, which is an important pillar of modern portfolio theory and one that we implement in our investment process. According to this theorem, the creation of an optimal portfolio involves two steps. First, we must develop a portfolio of shares irrespective of the risk tolerance of investors. The securities are selected solely on the basis of expected returns and will be reflected in the portfolio of all investors, regardless of their degree of risk aversion.

Second, we must complete the profile of the investor to determine their overall risk tolerance. At this point, we add less risky securities to the portfolio, such as bonds, in proportions that correspond to the level of risk aversion of the client. For example, a customer in their early forties could compose their portfolio of 75% equities and 25% bonds. The greater the desire to minimize risk, the higher the weighting of bonds will be. In other words, the low-risk securities establish the level of overall risk of the portfolio. The next step is to find the ideal combination of low- and high-risk securities in order to obtain the desired level of risk-tolerance. This optimal combination is determined on the chart below by the meeting point between the line representing all possible portfolios (from 100% in bonds to 100% in stocks) and the curve, which represents the risk tolerance of the investor concerned.

It should be noted that all investors have the same options, that is to say they have access to all possible portfolios on the market, while each investor has their own tolerance curve. Tobin has largely contributed to the composition of efficient portfolios, a practice that we adopted at Rivemont Investments. And if I happen upon the next Tesla or next Couche-Tard (yes, I admit having sold too early), all my clients will benefit; not just a few…

Market Prospects

| Subjet | Question | Recommendation | Comments |

|---|---|---|---|

| Allocation between equities and fixed income securities. | Est-ce les actions ou les obligations qui sont les plus intéressantes ? | Répartition neutre relativement aux indices de référence. | La hausse des taux d’intérêts se fait toujours attendre et le marché des actions s’est apprécié de façon substantielle. |

| Distribution between Canadian, U.S. and international. | Lesquelles des actions canadiennes, américaines ou internationales sont les plus intéressantes ? | Préférence pour le marché canadien et les marchés internationaux. | Certains marchés émergents pourraient amorcer une tendance haussière au cours des prochains mois. |

| Distribution between corporate bonds and government bonds. | Lesquelles des obligations de sociétés ou d’État sont les plus intéressantes ? | Recommande les obligations de sociétés plutôt que les obligations gouvernementales. | Nous recommandons les obligations corporatives de courtes et moyennes échéances ainsi que les obligations à haut rendement. |

| Investments in Canadian dollars or in foreign currency. | Les placements en devises augmenteront-ils ou diminueront-ils les rendements totaux ? | La progression du dollar canadien devrait être modeste et insuffisante pour décourager la diversification à l’étranger. | Aucun mouvement matériel du dollar canadien n’est prévu à moyen terme. |

Favorite Securities

You will find below a list of the eight individual securities with the largest weight in our “growth” portfolio. These stocks were selected based on their respective potential to outperform the stock market. You will find a short description of their activities, the annual dividend, if any, and the total return since their first inclusion in our portfolio.

Dated : July 25, 2014.

1 – RBCSymbol: RY |

5 – Alliance Grain TradersSymbol: AGT |

2 – Packaging Corporation of AmericaSymbol: PKG |

6 – Financière Sun LifeSymbol: SLF |

3 – SterisSymbol: STE |

7 – Globe Specialty MetalsSymbol: GSM |

4 – MonsantoSymbol: MON |

8 – AK SteelSymbol: AKS |

Conclusion

The trend for markets is still clearly on the rise. We are maintaining our current weighting in stocks and slight underweight in bonds. It will likely be difficult to beat the benchmark since our return to the Canadian markets (the Canadian exchange is our benchmark), but we believe that our effective methods for selecting stocks will continue to produce the results to which you are accustomed.

I would like to take this opportunity to thank Marie-Ève, who worked with us for part of the summer, and wish her the best of luck in pursuing her studies and in obtaining her CFA certification. Marie-Ève was very helpful and efficient. Moreover, some of the equities that we are monitoring are the direct result of her research and analysis.

Finally, if you are not one our clients, do not hesitate to contact us so that we can work together to see how a modern and personalized approach can help you achieve your financial goals.

Sincerely,

Martin Lalonde, MBA, CFA

President